Part 2: Is LL Flooring A Good Speculation?

Update on this post a week ago: Is LL Flooring A Good Speculation?

Bleecker Street Research answers with an emphatic “no!”.

God bless prudent short sellers and keep them safe, I say, so while I’m always reticent to stand opposite the bears that’s what makes a market, and in this case we’re coming at it from very different angles as is plainly obvious if reading both links above.

What I hadn’t mentioned previously:

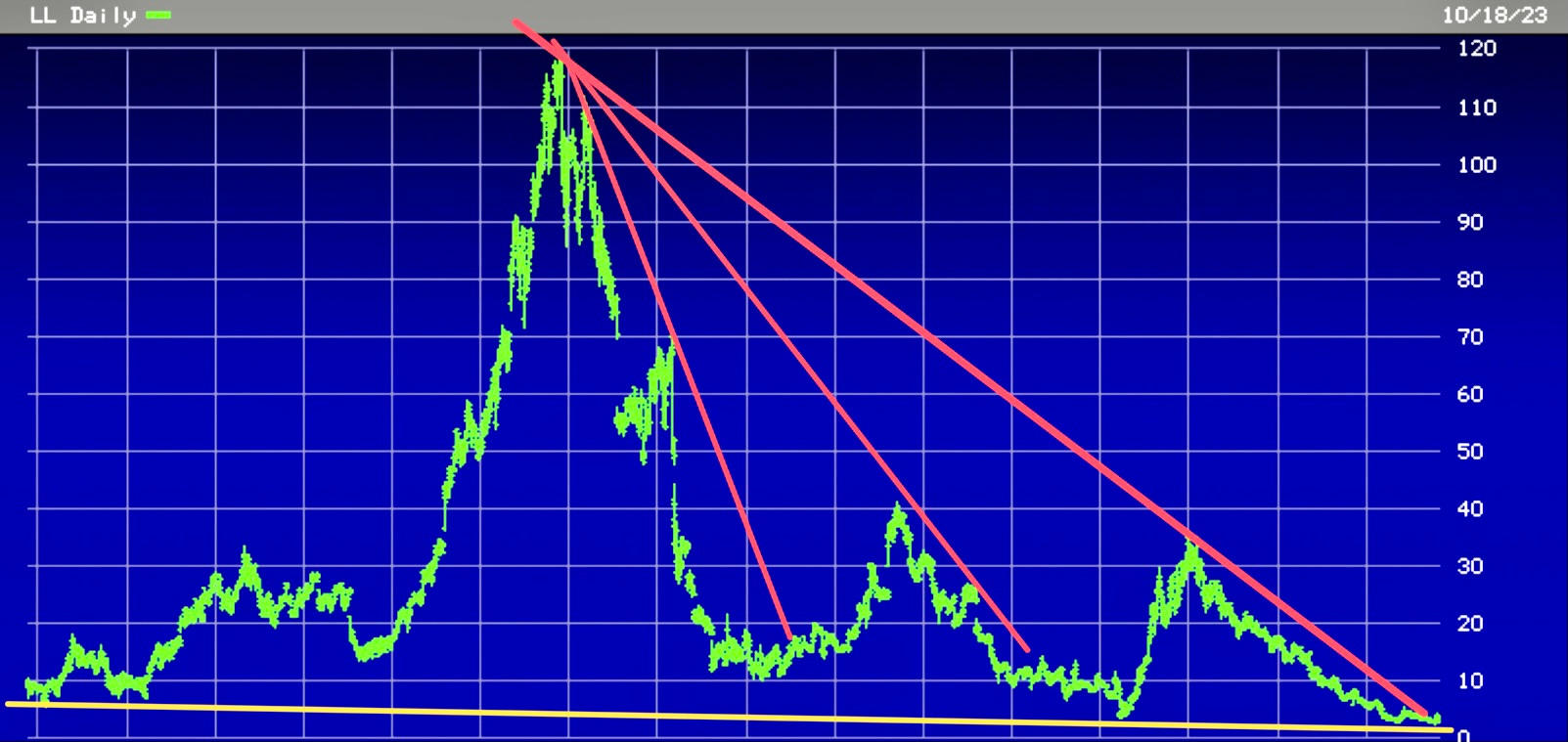

a 10-year down trend was about to be broken

buyout potential

LL rallied as much as 36% the day after my post, breaking a 10-year down trend:

Reasons for buyout speculation:

LL Flooring Board of Directors Unanimously Rejects Unsolicited Proposal - "The Board unanimously determined that the proposal significantly undervalues the worth of LL Flooring...”

My average cost is $3.33 on a double-sized position.

If LL tanks on November 1st, the day of its earnings report, I’ll double my position on that day and / or add another double position if or when it rallies either above its close of October 31 or in any case if it’s above $3.35 up to a limit of $3.75 after its earnings report.

My reasons are based on technicals showing a fantastic hit rate as detailed previously, with the added potential of a buyout at a higher share price.

In case of a buyout, trimming costs and/or selling some assets could make this a compelling turnaround play over the next couple years.

We’ll see, and I’ll post updates as the story unfolds.

Great stuff. And great room you ran in Clubhouse discussing this!